Quantitative Understanding of the Trickle-Down Hypothesis (Amazon Kindle)

We obtained quantitative result that is the exact opposite of the trickle-down hypothesis.

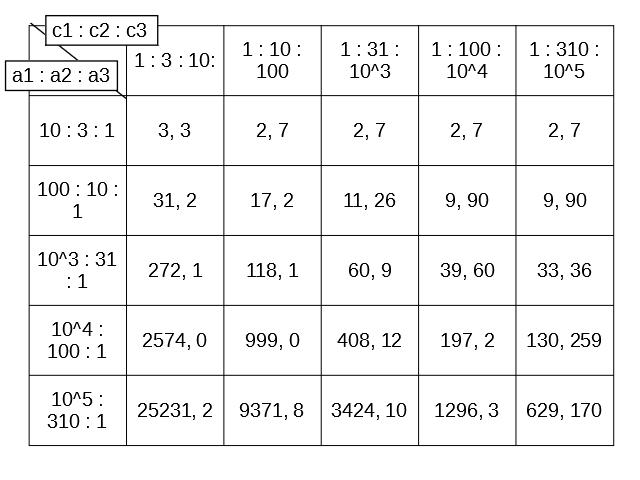

For studying trickle-down, we performed an estimation of the circulation of the money flow only between business and households. Business is divided into small, middle, and large companies, and households are divided into low-, middle-, and high-income earners. In this estimation, we obtained numbers of small and middle companies that a high-income earner needs for trickle-down. Free parameters of our estimation are the income ratio and the number ratio of the low-, middle-, and high-income earners in a large company.

As a result, the larger the income ratio is, the more companies the high-income earner needs for trickle-down. This makes trickle-down difficult in the modern economy. This tendency quantitatively denies the trickle-down hypothesis that `if the wealthy become more rich, people obtain benefit via consumption by the wealthy.'

In this table, (a1: a2: a3) indicates the income ratio of the high-, middle-, and low-income earners, and (c1: c2: c3) indicates the number ratio of the high-, middle-, and low-income earners in a large company. A criterion for judging the magnitude of these numbers is 104 days, the number of days per year on Saturday and Sunday.

===

Table of Contents

Chapter 1 Introduction

Chapter 2 Estimation

2.1 Outline of our estimation

2.2 An example of estimation

2.3 Parameter survey

2.4 Directors of real large companies

Chapter 3 Discussion

3.1 Dysfunction of trickle-down

3.1.1 Ideal, time, and reality

3.1.2 Temporal limit

3.1.3 A psychological barrier

3.1.4 High-income earners = vulnerable consumers

3.2 Improvement of our estimation model

3.2.1 Introduction

3.2.2 Other economic agents

3.2.3 Diversification of our company model

3.3 The analogy of a glass tower and wine

3.4 Real money flow

Chapter 4 Summary

References

No comments:

Post a Comment